All you need to know about dollar cost averaging

One dilemma you'd likely face when you're mapping out your wealth strategy is whether you should invest your money in smaller, regular amounts, or if you should make a big splash and sink all your money in at one go.

If you're a novice investor or are uncertain about how the market is likely to move, the practice of making smaller, steadier investments might be a good place to start. This investment method is called dollar cost averaging. Let's explore it a little further.

So, what is dollar cost averaging?

Picture yourself on a roller coaster. Slowly rising up to the heights... then plunging down to the ground before you start the next climb. Very exciting for an afternoon ride. Not so much fun for your investments - this market volatility can cause a fair degree of anxiety, especially if you don't quite yet have the financial experience to be able to predict how the tide may go.

How does dollar cost averaging work? It can help you smooth out these highs and lows caused by short-term market volatility. It lets you make smaller investments at regular intervals, as the roller coaster goes up and as it comes down, so you can avoid making one lump-sum investment at what may be an inopportune moment.

Why choose dollar cost averaging?

- Easier decision making

If you take a look at any stock market chart, you'll see that prices go up and down all the time - it truly is a roller coaster out there. Dollar cost averaging means you don't have to worry about perfectly timing every trade. You can take a less emotional, less stressful, more hands-off approach because it averages out the asset price you pay in the short to medium term. And let's face it, most of us lack the expertise and resources to constantly evaluate whether it's the best time to invest in a particular stock, so it's great if we can save ourselves from constantly worrying about making sub-optimal decisions when navigating the markets. - Lower risks with your capital and investment journey

With dollar cost averaging, it means you'll be investing the same amount each month. When stock prices are higher, you get fewer shares; and when prices drop, that fixed amount buys you more shares. It reduces the risk of dropping a huge lump sum at the wrong time. You won't be left worrying even if there are price fluctuations the next day or week; with this disciplined approached, your regular investments can help to average out the stock price over time.

And you don't just benefit from averaging out the unit price. By adopting a long-term investment plan, you can also seize the opportunity to 'buy low' during recession periods, and reap the rewards when the markets recover. These steady investments mean you literally get the best of both worlds and peace of mind, too, while you're at it. - Lower barriers to entry

You might think you need a huge amount of capital to begin investing and that could deter you from even starting, but that doesn't need to be the case. If you invest in unit trusts, you can actually get started with SGD1,000 as an initial deposit and then make steady, manageable monthly investments of just SGD100 after that. You'll even get a professional fund manager to choose shares from different companies for your investment bundle. That way, you'll benefit from not having to do your own extensive research on those companies and your investment is also diversified enough so if you've got one stock that is underperforming, your entire balance won't be as adversely impacted.

Do these strategies work all the time? Like all investment methods, it's good to have a balanced understanding of the full picture, so let's take a look at some cons to dollar cost averaging.

- If you've got a persistently underperforming stock, even dollar cost averaging won't help much with your returns, so it's still important to at least do some research on the companies and stocks you invest in.

- Making smaller, regular investments means there are more transactions involved. Usually, that means you will be charged higher fees for each transaction, instead of just a single fee if you make a lump sum investment. But at HSBC, we offer promotions from time to time that can ease such transaction costs or help you earn additional rewards as you invest.

- When the market is on a strong bull run, dollar cost averaging might not provide you the best bang for your buck. If financial markets are demonstrating a consistently strong uptrend, then you will likely get a higher return on investment if you make a lump sum investment in stocks, instead of doing it in smaller intervals.

Now that you've gained a better understanding of dollar cost averaging, let's take a look at the other investment method we just mentioned: lump sum investing.

What is lump sum investing?

If you've built up your cash reserves and feel confident enough that your target stock is now 'cheap' enough, you could make invest a single sum of money in it at one go - that's called lump sum investing. The good news is - if you get it right, your return on investment could really be worth your while. If you're adept at tracking prices and experienced enough to take stock of market trends to determine the best time to invest, then this might be a good method to explore. But the downside is - it's difficult to time the market and be absolutely confident that a stock price is cheap enough for you to go all in for. Lump sum investing could also potentially bring about quite a bit of stress or nerves, as you have to constantly keep your eye on the market and monitor stock prices.

Dollar cost averaging vs lump sum investing

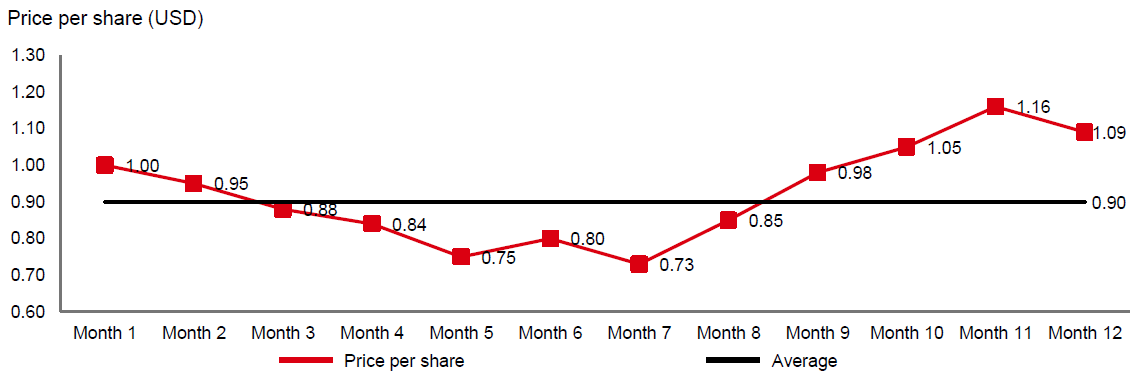

With that said, let's understand dollar cost averaging better. Imagine you're investing in Stock A, with a starting price of USD1.00. It goes up and down each month, and records a low of USD0.73 and a high of USD1.16 in the span of a year1.

Would you:

- A) make a lump-sum investment in month 1 or;

- B) invest USD1,000 every month over 12 months

If you chose option A to make a lump sum investment, you'd get 12,000 shares. And at the end of the year, your investment would gain 9% in value, or USD1,080.

If you chose B to invest USD1,000 each month, you'd get 13,257 shares, paying an average of USD0.90 per stock. By using dollar cost averaging, your portfolio in turn is up 20% over a 12-month investing period, or USD1,360, taking into account a current stock price of USD1.09. That means your smaller, regular investments have given you higher returns than if you had made a lump sum investment.

This strategy doesn't always outperform compared with someone who times the market correctly to make a lump sum investment, but as you can see the price was below USD0.90 just 6 months in that year. In this case, that means there's only a 50% chance for lump-sum investments to edge out!

Ultimately, you have to weigh it out to see if dollar cost averaging or lump sum investing is a better fit for your investment risk appetite. And it doesn't just have to be one or the other: you could also choose to invest using a mix of both approaches. For example, you can use dollar cost averaging to build up your investments on a regular basis and make lump sum investments during market downturns when you feel there is a good opportunity to 'buy low', or what is called going long. Either way, it is important to take a long term view for your investment strategy and start being proactive at making your money work for you.

Ready to get started?

If you already have an investment account,

Don't have an account yet? We can help get you started.